If you’re one of the many small business owners who applied for the Paycheck Protection Program, known as the (PPP), you’ll want to know how getting that loan forgiven actually works.

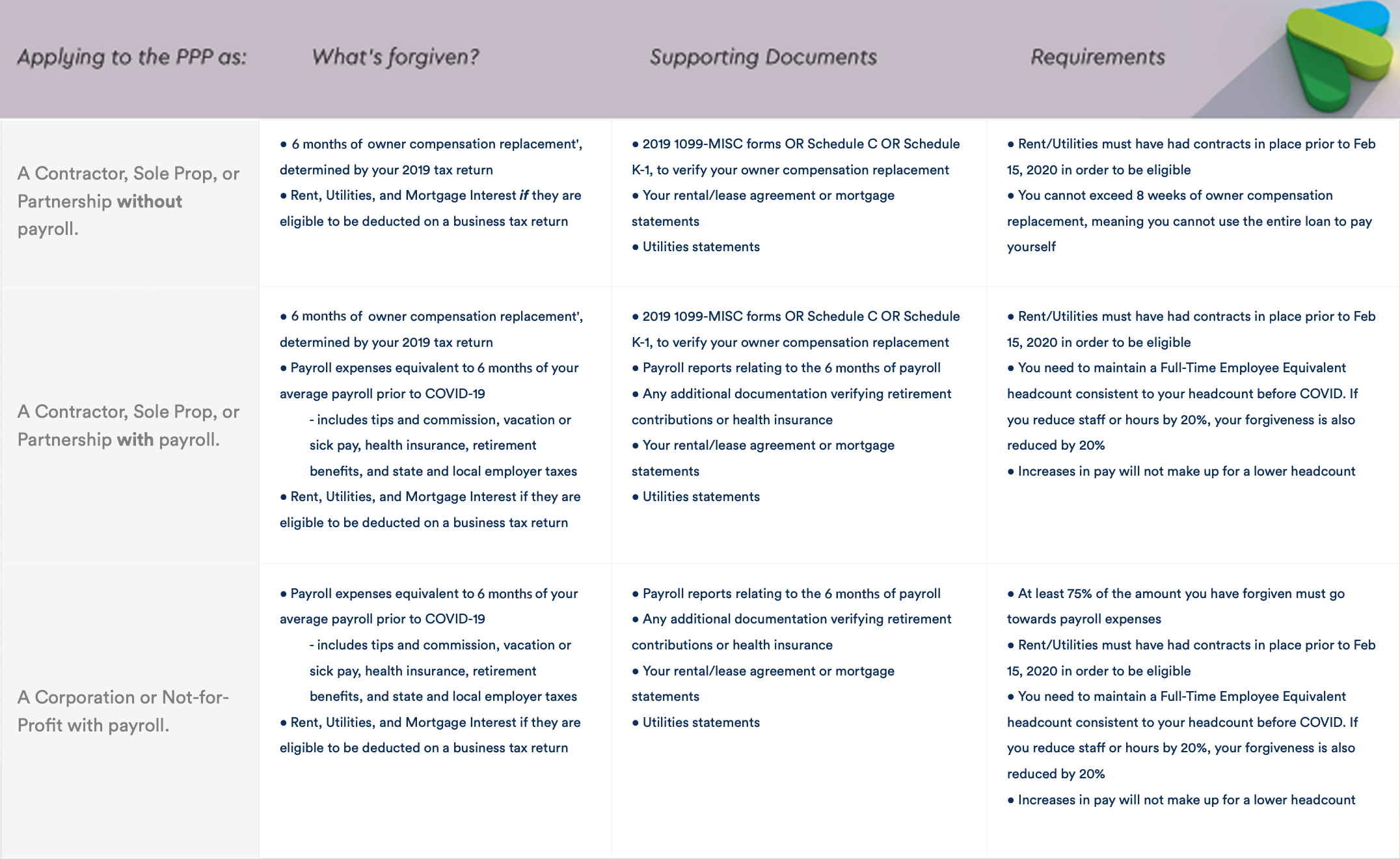

In short, borrowers will have their loans forgiven if they use the money for designated expenses. Total payments for payroll over the 6 months after the loan is disbursed may be forgivable. Mortgage interest, rent, and utilities are also forgivable, up to 40% of the PPP loan.

The loan amount is based on your average monthly payroll cost for 2019. You can receive 2.5 times that amount, to help cover 6 months of payroll. As long as you use the loan amount appropriately, you can have the loan forgiven.

The funds from the PPP can be used for the following purposes:

- Payroll—salary, wage, vacation, parental, family, medical, or sick leave, health benefits

- Mortgage interest—as long as the mortgage was signed before February 15, 2020

- Rent—as long as the lease agreement was in effect before February 15, 2020

- Utilities—as long as service began before February 15, 2020

Here’s Guidance on Getting Full Loan Forgiveness!

To review all the details of the loan forgiveness guidelines click here and download a PPP loan forgiveness application.

PPP FAQ’s

Can I get PPP expenses forgiven and deduct them from my taxes?

No. Any expense you claim for forgiveness under the PPP can’t be deducted from your expenses. A forgivable PPP loan is already tax-free, so the IRS wants to prevent double-dipping (getting free money from the same source twice).

What counts as a utility expense?

Business expenses on electricity, gas, water, transportation, telephone, or internet access are eligible uses of PPP funds and qualify for forgiveness.

My bills are due outside the 8-week covered period. Can I claim these expenses?

This is a moot point since the Senate (as of 6/3/20) passed a bill extending the time frame from 8 weeks to 26.

How long do I need to keep my documents?

You must hold on to supporting documents for (6) six years after the loan is fully forgiven or entirely repaid, and provide them to the SBA or the Office of Inspector General if and when requested.

Related Articles

Edison Partners Leads $115M Growth Investment in Fingercheck

New capital infusion and appointment of highly experienced CEO to accelerate growth of end-to-end deskless workforce management platform. NASHVILLE, Tenn. & PRINCETON, N.J.–Growth equity investment…

Fingercheck Announces Integrated Work Opportunity Tax Credit Service, Powered by WOTC.com

Fingercheck Clients Are Now Able to Leverage Lucrative Federal Hiring Credits BROOKLYN, NY, July 17th, 2024 – Fingercheck, is excited to announce the launch of…

Project W: Q&A with Tiffany Haynes, COO of Fingercheck

Tiffany Haynes, the Chief Operating Officer of Fingercheck, is a recognized leader in the fintech sector. Not only does she run a rapidly growing company, but…